宮城(仙台)の絶対すぐ借りれる街金!

激甘審査でブラックでも借りれる街金、おすすめ17社。

「お金を借りたいけれど、どこからも断られてしまった…」

そんな悩みを抱えていませんか? 銀行や大手消費者金融は審査が厳しく、信用情報に傷があると融資を受けるのが難しくなります。

特に、フリーランスやアルバイトの方、過去に滞納歴がある方にとっては、高い審査基準が大きな壁となるでしょう。

そんなときに頼りになるのが「街金」と呼ばれる貸金業者です。

この記事では、宮城(仙台)で利用できる「激甘審査」の街金について、以下のポイントを詳しく解説します。

- 大手金融機関と街金の違い

- 街金の審査基準や特徴

- 在籍確認の有無や対応方法

- 総量規制を超えても借入が可能か

- 即日融資を受けるための手順

- 街金と違法業者(闇金)を見分ける方法

これらの情報を知ることで、安心して利用できる街金を見つけ、スムーズに融資を受けるための知識を得ることができます。

- 宮城(仙台)の街金!即日融資のブラックでも借りられる消費者金融一覧

- 1.クレジットカード現金化【プライムウォレット】選ばれ続ける超優良店

- 2.クレジットカード現金化【インパクト】最短5分で振込完了

- 3.クレジットカード現金化【あんしんクレジット】業界最高クラスの還元率

- 4.クレジットカード現金化【Quick現金サービス】とにかく早い!

- 4.クレジットカード現金化【どんなときもクレジット】初めての方、換金率3%UP

- 【QUICK39】お金を貸してくれるところをご紹介

- 1.【フクホー】ゆとりのローン!安心の金利7.30%〜

- 2.【スカイオフィスキャッシング】スピードと信頼の消費者金融

- 3.【キャレント】で借りんと!融資申込みキャンペーン中!

- 4.【アロー】最短即日融資もOK

- 5.【アルコシステム】信頼と実績のキャッシング

- 6.【プラン】全国どこからでも24時間簡単ご契約

- 7.【クレジットのニチデン】簡単・便利なネットキャッシング

- 8.【いつも】いつものキャッシング

- 9.借りやすくて返しやすい!キャッシング【フタバ】

- 10.来店不要・振込キャッシング【パーソナルクレジット セントラル】

- 11.安心できるパートナー【ハローハッピー】フリーローン

- 12.来店不要・振込キャッシング【女性専用 マイレディス】

- 女性専用!在宅で稼ぐ【FANZAノンアダルトチャットレディ募集】

- 宮城(仙台)の街金|サービス対象地域について

- 宮城(仙台)の激甘審査の街金を探すときの注意点

- 宮城(仙台)の激甘審査の街金は審査が甘い

- 宮城(仙台)の激甘審査の街金は在籍確認なしか

- 宮城(仙台)の激甘審査の街金は総量規制オーバーでも借りれるか?

- 宮城(仙台)の激甘審査の街金で即日融資を受けるには

- 宮城(仙台)の激甘審査の街金と、闇金との違い

- 宮城(仙台)の激甘審査の街金で審査落ち・・お金を借りれないときは

宮城(仙台)の街金!即日融資のブラックでも借りられる消費者金融一覧

かんたんアンケートに答えるだけで、おこづかいをゲット

| 無料会員登録!アンケートに参加するだけで、お小遣い稼ぎ |

|||

| サービス名 | サービス内容 | 報酬額 | 無料登録 |

| 【マクロミル】 |

スマホやPCで手軽にアンケートに答えて「現金」や「電子ギフト券」に交換可能なポイントがもらえます! | 新規登録で最大1000ポイント!(1,000円相当) | \会員120万人/ |

【オピニオンワールド】 |

かんたん登録1分、会員登録無料!ポイントを現金かギフトカードに交換 | アンケート1回につき、最高900円! | \900円ゲット/ |

【ボイスノート」】 |

かんたん登録1分、アンケート参加でポイントを現金かギフトカードに交換 | 会員登録だけで70ポイント獲得! | \今すぐ登録/ |

【モニタータウン |

かんたん登録1分、設定5分、会員登録無料!現金かギフトカードに交換 | アプリインストールでポイント獲得(2,800円相当) | \iphone専用/ |

【モニタータウン |

かんたん登録1分、設定5分、会員登録無料!現金かギフトカードに交換 | アプリインストールでポイント獲得(2,800円相当) | \Android専用/ |

【モニタータウン】 |

かんたん登録1分、設定5分、会員登録無料!現金かギフトカードに交換 | アプリインストールでポイント獲得(900円相当) | \PC専用/ |

【ハピタス】  |

お買い物やサービスの申し込みでポイントを貯めて、現金やギフト券に交換 | 会員登録時・500ptをプレゼント | \会員80万人/ |

スマホと紹介コードが必須!

スマホで銀行口座を開設するだけでおこづかいゲット!

| かんたん!【スマホ専用】無料の銀行口座開設でお小遣いをゲット | |||

| 銀行名 | 報酬額 | 紹介コード | 無料口座開設(スマホ必須) |

第一生命NEOBANK |

¥1,500 |

oFFWZro |

第一生命NEOBANK |

みんなの銀行 |

¥500 | hYBchqNL | みんなの銀行 |

UI銀行 |

¥500 | sh4402 | UI銀行 |

女性限定のお金稼ぎ!

在宅OKのかんたん美容モニタや、チャットレディ

| 【女性限定】かんたん!即金!お小遣い稼ぎができる在宅ワーク | |

【女性専用!美容モニター】 |

エステだけでなく、コスメや健康食品などを試せる在宅ワークのモニターも多数!「ファンモニ」(無料)会員登録はこちら 謝礼は1件1000円~5,000円ほど、複数組合わせれば月4万円以上も可能 |

【女性専用!在宅で稼ぐ】 |

自分の好きなタイミングで稼げるFANZAの在宅チャットレディ! ノンアダルトだから安心!スマホでかんたん在宅ワーク 時給7,500円以上可、安心の個人情報対策、最短翌日振込! |

ファクタリングなら!

あなたの持っている債権を買取ります!

| ファクタリング | 即日融資 | 手数料 | 申込み |

1.アクセルファクター |

来店不要 最短2時間!即日融資 |

買取手数料0.5%~ 審査通過率 93.3%以上 |

\個人・法人/ |

2.資金調達プロ |

かんたん10秒! 無料診断 最短即日融資 |

提携事業者数No1! 資金繰り改善率93%以上 |

\個人・法人/ |

3.株式会社No.1 |

最短30分で即日振込可能 | 買取手数料1%~(業界最安) 審査通過率 90%以上 |

\個人・法人/ |

4.エスコム |

最短即日で審査完了。 即日に資金調達可能。 |

1.5%〜12% 資金化成功率97% |

\個人・法人/ |

5.Easy factor |

最短10分でお見積り 最短60分で振込可能 |

2%〜8% 資金化成功率97% |

\個人・法人/ |

6.いーばんく |

来店不要 最短即日入金可能 |

買取手数料4%~ 審査通過率 90%以上 |

\個人・法人/ |

7.ジャパンマネジメント |

最短即日で審査完了。 翌日に資金調達可能。 |

三社間(3%~10%) 二社間(10%~20%) 資金化成功率93% |

\個人・法人/ |

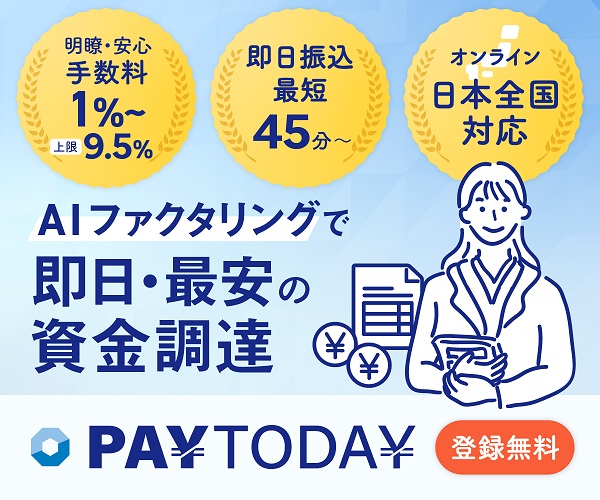

8.PayToday |

最短30分で審査完了。最短45分で振込可能。 | 1%〜9.5%(上限) | \個人・法人/ |

9.MSFJ |

来店不要 最短1日で買取可能 |

1.8%〜9.8% 累積実績1万件以上 |

\個人・法人/ |

10.トラストゲートウェイ |

来店不要 最短即日振込 |

1.5%〜9.5%(業界最安水準) 審査通過率95% |

\個人・法人/ |

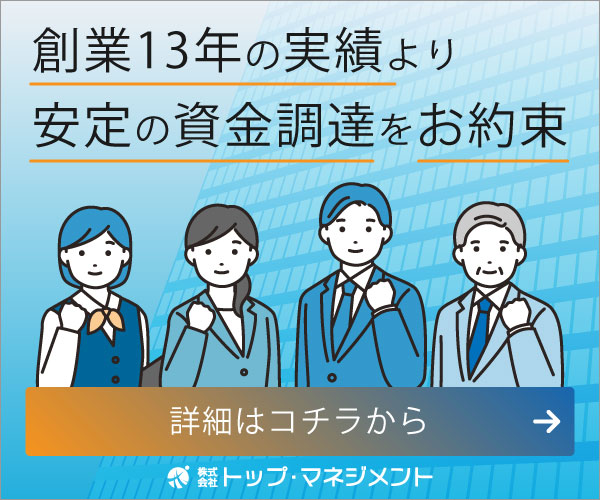

11.トップ・マネジメント |

来店不要 最短即日振込 |

3社間ファクタリング(買取対象債権の99.5%〜96.5%) 2社間ファクタリング(買取対象債権の96.5%〜87.5%) |

\個人・法人/ |

12.西日本ファクター |

最短即日即買取り 診断無料 |

【九州、中国、四国エリアに限定】 手数料は2.8%〜 |

個人・法人(九州、中国、四国) |

13.三共サービス |

来店不要 資金化まで最短翌日 |

平均手数料8% 資金化成功率97% |

\法人のみ/ |

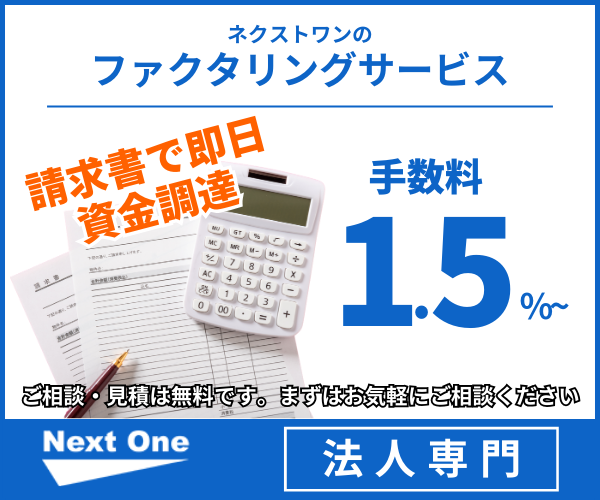

14.ネクストワン |

来店不要 資金化まで最短即日 |

1.5%〜10%(業界最安水準) | \法人のみ/ |

15.ラボル |

来店不要 最短30分入金 |

買取額の10% 振込手数料などの費用なし |

\個人事業主のみ/ |

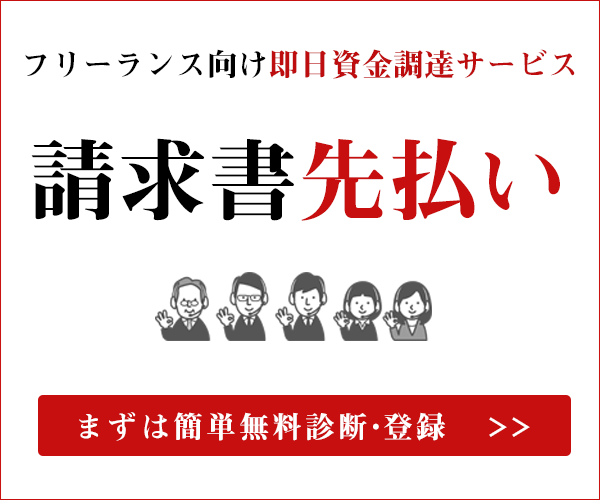

16.請求書先払い |

最短60分でお振込み 対面不要 |

手数料3%〜10% 最低買取金額10万円 |

\個人事業主のみ/ |

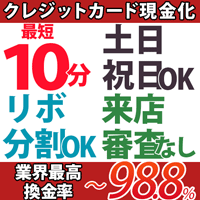

クレカの現金化サービスなら、即日にも対応してくれます!

| 社名 | 即日融資 | 実質年率 | 限度額 | 特徴 |

| 1.クレカ現金化「プライムウォレット」 |

最短10分 | 還元率最大98% | 設定なし | ・24時間受付 ・土日祝日も即日振込 ・カード事故過去0件 |

2.クレカ現金化「インパクト」 |

最短5分 | 還元率最大99.5% | 設定なし | ・審査不要 ・土日祝日も即日振込 ・来店不要 |

3.クレカ現金化「あんしんクレジット」 |

最短3分 | 還元率最大99.5% | 設定なし | ・審査不要 ・土日祝日も即日振込 ・来店不要 |

4.クレカ現金化「Quick現金サービス」 |

最短20分 | 還元率最大90%(手数料無料) | 設定なし | ・24時間365日受付 ・土日祝日も即日振込 ・審査不要 |

5.クレカ現金化「どんなときもクレジット」 |

最短5分 | 還元率最大98% | 設定なし | ・24時間受付 ・土日祝日も即日振込 ・スマホで申込完結 |

QUICK39のキャッシングローン紹介 |

お金を貸してくれるトコロを見つけます。 どこからも借りれない・・金利が高くもっと安いところへ借り換えしたい・・こんな悩みを解消します。 |

・完全無料 ・紹介料無料 ・手数料無料 |

||

1.フクホー |

対応 | 7.3%〜18.0% | 1〜200万円 | ・24時間受付 ・来店不要 ・利息は利用日数分だけ |

2.スカイオフィスキャッシング |

対応 | 15.0%〜20.0% | 1〜50万円 | ・24時間受付 ・来店不要 ・最短30分で審査完了 |

3.キャレント |

対応 ※ | 7.8%〜18.0% | 1万円~500万円 | ・24時間受付 ・来店不要 ・申込まで3分で完了 |

4.アロー |

対応 | 15.0%〜19.94% | 200万円まで | ・24時間受付 ・来店不要 ・かんたん3秒診断 |

5.アルコシステム |

対応 | 15.0%〜20.0% | 1〜50万円 | ・24時間受付 ・来店不要 ・保証人・担保不要 |

6.プラン |

対応 | 12.00%~18.00% | 1〜50万円 | ・24時間受付 ・来店不要 ・保証人・担保不要 |

7.クレジットのニチデン |

対応 ※ | 7.3%〜17.52% | 1〜50万円 | ・24時間受付 ・来店不要 ・100日間利息なし(初回のみ) |

8.いつも |

対応 | 4.8%~18.0% | 1万円~500万円 | ・24時間受付 ・来店不要 ・最大60日間利息なし(初回のみ) |

9.フタバ |

対応 | 14.959%~19.945% | 1万円~50万円 |

・24時間受付 |

10.セントラル |

対応 |

4.8%~18.0% |

1万円~300万円 | ・24時間受付 ・最大30日間利息なし(初回のみ) ・セブン銀行ATMでご利用ご返済が可能 |

11.ハローハッピー |

対応 | 10.00%~18.00% | 100万円まで | ・24時間受付 ・来店不要 ・保証人・担保不要 ・パート・アルバイト・主婦の方も歓迎 |

12.マイレディス |

対応 | 4.80%〜18.00% | 1万円〜100万円 | ・24時間受付 ・来店不要 ・保証人・担保不要 ・女性専用キャッシング |

| 【女性専用!在宅で稼ぐ】 |

自分の好きなタイミングで稼げるFANZAの在宅チャットレディ! ノンアダルトだから安心!スマホでかんたん在宅ワーク 時給7,500円以上可、安心の個人情報対策、最短翌日振込! |

|||

13.オージェイ |

対応 | 9.5%〜18.0% | 10万円~5,000万円 | ・24時間受付 ・来店不要 |

14.アクト・ウィル |

対応 | 7.5%〜15.0% | 300万円~1億万円 | ・24時間受付 ・来店不要 ・審査は最短60分 |

15.ファンドワン |

対応 | 2.5%〜18.0% | 30万円~1億円 | ・24時間受付 ・来店不要 ・審査は最短40分 |

16.MRF |

対応 | 4%〜15.0% | 30万円~3億円 | ・24時間受付 ・来店不要 ・24時間以内に仮審査 |

※ 平日14時までの手続完了が条件

激甘審査の絶対すぐ借りれる街金(消費者金融)をご紹介します。

どの消費者金融も独自審査を採用しており、柔軟な対応をしてくれるのでブラックでも借りれて即日融資OKの可能性が高いです。

ブラックだからと諦めずに真剣にお金が必要な理由を説明して少しでも融資をしてもらえる確率をあげましょう。

またクレジットカードを現金化してくれる優良サービス店も合わせてご紹介します。

1.クレジットカード現金化【プライムウォレット】選ばれ続ける超優良店

ショッピング枠現金化業界で超有名で誰もが知っているプライムウォレット!

現在日本でも、キャッシュレス化が進んでおりクレジットカードを保有する方は増えておりますね♪

15時以降でも即日振込み可能で、地方銀行もOKです。

2.クレジットカード現金化【インパクト】最短5分で振込完了

インパクトは、超高還元率(最高99.5%)でしられるクレジットカード現金化優良店です。

さらに新規申込で2%換金率UP!

審査不要、来店不要で最短5分でお振込み。

クレジットカードのショッピング枠があれば現金化してくれる安心の優良店です。

3.クレジットカード現金化【あんしんクレジット】業界最高クラスの還元率

あんしんクレジットは、超高還元率(最高98.8%)でしられるクレジットカード現金化優良店です。

審査不要、来店不要で最短5分でお振込み。

クレジットカードのショッピング枠があれば現金化してくれる安心の優良店です。

4.クレジットカード現金化【Quick現金サービス】とにかく早い!

Quick現金サービスは、振込金額を最初に提示する優良現金化サービスです。

24時間WEB対応やLINEチャットなど、お客様目線のサービスを提供し続けてリピーターは脅威の90%以上!

急な出費でお金が足りない!そんな方でも大丈夫!

4.クレジットカード現金化【どんなときもクレジット】初めての方、換金率3%UP

急な出費で困っていませんか?

どんなお悩みも、どんなときもクレジットにお任せください。

お申込みが初めての方なら換金率3%アップ!

審査不要、来店不要で今すぐ現金化してくれる安心サービスです。

【QUICK39】お金を貸してくれるところをご紹介

消費者金融からの借り入れが多数あってどこからも借りれないと思っている方や 金利が高くてもっと安いところへ借り換えしたい方・・・

このような悩みを抱えたお客様にたいして 安心して安全でより安く借り入れが出来るようにサポートさせていただいております。

完全無料ですのでお客様から紹介料・手数料等の料金は一切いただいておりません。

1.【フクホー】ゆとりのローン!安心の金利7.30%〜

★創業45年★

キャッシング・消費者金融のフクホー 安心の金利7.30%〜!

最高200万円までのゆとりのローン。

キャッシング・消費者金融・ローンなら創業45年のフクホー。

ご来店一切不要、振込み キャッシングの消費者金融です。

レディースキャッシングもご用意しているので、女性の方でも安心してご利用頂けます。

2.【スカイオフィスキャッシング】スピードと信頼の消費者金融

最短30分!来店不要 スピードキャッシング!!受付は24時間可能!

当日 9:00〜14:00 までにお申込み頂きますと、 即日のお振込みが可能です。

スカイオフィスニッセイキャッシングは他社で断られた方でも柔軟に対応している消費者金融です。

インターネットから申込みを行い、審査が完了すればその日に融資を受けられます。

来店不要のスピードキャッシングは急な出費でお困りの方の力強い味方です。

3.【キャレント】で借りんと!融資申込みキャンペーン中!

インターネット専用キャッシング♪完全非対面でネット完結。

カード発行不要!全国どこでもご指定の銀行口座にお振込み致します。

担保、保証人不要でキャッシングが可能です。

インターネット申込み、365日、24時間受付中!

申込フォームの入力内容が少なく、簡単にお手続きいただけます♪

ご利用限度額は【1万円〜500万円】まで。

大手消費者金融、カードローンの審査が通らなかった方でも柔軟な審査で対応致します。

4.【アロー】最短即日融資もOK

無担保かつスピーディーな使途自由ローンです。

・独自審査

・来店不要

・最短即日振込

・アプリならWEBで完結、郵送物は一切なし!

「郵送物が一切不要なアローWEB完結ローン」の取扱いを開始いたしました。

お申込み後、一次審査が通過した方は、スマホでアプリをダウウンロードして頂くことで、 サービスをご利用いただくことができます。

5.【アルコシステム】信頼と実績のキャッシング

創業1983年、信頼と実積、振込キャッシングの老舗です。

お申し込み後、最短でその日のうちにご指定口座に送金いたします。

貸付利率(実質年率) 年3.00%~20.00%

保証人・担保不要。

ご融資範囲 50万円まで(要審査)

お申し込みはWEBで、24時間受付中。

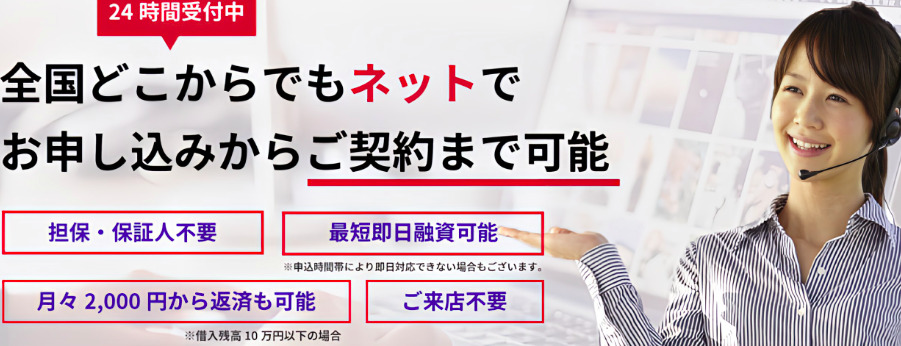

6.【プラン】全国どこからでも24時間簡単ご契約

全国どこからでも24時間ネットでお申し込みからご契約まで可能です。

又、キャッシュサービス『プラン』では1万円から最高50万円までご融資可能です。

・ご来店不要

・最短即日ご融資可能

・担保・保証人不要

・月々2,000円からのご返済も可能

7.【クレジットのニチデン】簡単・便利なネットキャッシング

簡単・便利・ネットキャッシング ニチデンのネットキャッシングへようこそ。

簡単・便利・ネットキャッシング ニチデンのネットキャッシングへようこそ。

振込ローン・不動産担保ローン・事業者ローンをご用意しています。

学生ローンにも対応、20歳以上で定期的に収入のある方を対象としております(パート・アルバイト・主婦の方も歓迎します)

大学生〜幅広い層に対応しており、福山、福山と3店舗ありますので手厚いサービスをモットーとして運営しています。

8.【いつも】いつものキャッシング

『早い』 来店不要!24時間申込受付、最短45分でお振込完了。

『頼れる』ご利用は1万円〜最大500万円まで。

『便利』 カード発行不要!郵送物一切なし!お客さまに合わせた柔軟な在籍確認。

『安心』 LINEやメール・電話でご対応、ご融資まで完全サポート。

『納得』 電話応対コンクールにて数度入賞した丁寧なご対応。

9.借りやすくて返しやすい!キャッシング【フタバ】

創業50年以上の実績と信頼のキャッシングのフタバです。

・来店不要・即日振込みキャッシングです。

・インターネット申込みで24時間全国受付

・お申込みはとっても簡単、お申込みフォームに入力するだけ。

・過去に自己破産・債務整理等された方もまずはお申込みください。

・大手消費者金融やカードローンの審査が通らなかった方もお申込みください。

・女性スタッフが対応致します。

10.来店不要・振込キャッシング【パーソナルクレジット セントラル】

<<創業40年を超える安心と実績の「セントラル」>>

WEB申込で当日最短融資可能です!

全国の皆さまからのお申込みに対応いたします。

セントラルは昭和48年創業の老舗の貸金業です。

全国に17店舗展開しております。 東京都内4店舗(浅草、新橋、新宿、池袋)、埼玉と神奈川に各1店舗 愛媛6店舗、香川2店舗、高知1店舗、岡山2店舗 計17店舗展開。

全国のセブン銀行ATM提携を開始し、 全国の方々にもますますご利用していただきやすくなりました。

さらに、ご利用が初めての方は最大30日間金利0円!

11.安心できるパートナー【ハローハッピー】フリーローン

ハローハッピーは身近なキャッシング!

20歳以上で定期的に収入のある方を対象としております(パート・アルバイト・主婦の方も歓迎します)

家電ローン:家電製品のご購入

教育ローン:保育園〜大学の学費

リフォームローン:ご自宅の増改築・修理

医療ローン:入院、通院費 事業資金ローン

事業資金ローン:自営業、学資資金

ハローハッピーは各都道府県の方々へのサービスが手厚いお店です。

12.来店不要・振込キャッシング【女性専用 マイレディス】

<<創業40年を超える安心と実績の「セントラル」>>

そんなセントラルから生まれた女性専用のキャッシング【マイレディス】

WEB申込で当日最短融資可能です!

全国の皆さまからのお申込みに対応いたします。

中四国中心に店舗展開の老舗セントラルは、首都圏店舗も拡充中!

全国のセブン銀行ATM提携を開始し、 全国の方々にもますますご利用していただきやすくなりました。

さらに、ご利用が初めての方は最大30日間金利0円!

女性専用!在宅で稼ぐ【FANZAノンアダルトチャットレディ募集】

自分の好きなタイミングで稼げる在宅チャットレディ。

ノンアダルトだから安心、スマホで出来るかんたん在宅ワークです。

初めての方でも「業界最大手」「FANZAだから安心」してお仕事できます。

高収入在宅アルバイトならFANZAチャットガール!

隙間のお時間でお仕事可能、副業としても大歓迎です。

万全の個人情報管理、時給7,500円以上可、最短翌日振込!

宮城(仙台)の街金|サービス対象地域について

街金(消費者金融)は、急な資金が必要な時に頼りになるサービスです。

特に仙台市を中心とする宮城県では、急な出費に対する解決策として多くの人々に利用されています。

この記事では、宮城(仙台)の街金のサービス対象地域について、どのようなエリアでサービスを提供しているのか、また利用する際のポイントなどを詳しく解説します。

宮城(仙台)の街金とは?

街金(消費者金融)は、短期間で少額融資を提供する金融機関で、急な出費や予期しない経済的な負担に対応するために利用されます。銀行などの大手金融機関と比べると、審査が比較的緩やかで、申し込みから融資までの時間が短いことが特徴です。そのため、急な支払いが必要なときに非常に便利なサービスとなります。

仙台市をはじめとする宮城県内では、インターネットを利用したオンライン融資を提供している街金も多く、便利な方法で融資を受けられるのが特徴です。オンライン申込みを通じて、インターネットからいつでもどこでも融資を受けることが可能です。また、対面での相談ができる店舗も多く、柔軟にサービスを利用できる点も魅力です。

仙台市内のサービス対象地域

仙台市は宮城県の中心都市であり、数多くの街金が集まっています。仙台市内で提供される街金のサービスは、市内各区でアクセスしやすく、住民のニーズに応じた融資を行っています。特に、青葉区や宮城野区などは交通が便利で、多くの人が集まるため、街金のサービスを利用する人々も多いエリアです。

青葉区

青葉区は仙台市の中心地にあり、商業や行政の中心地としても知られています。このエリアでは、多くの街金がオフィスや店舗を構えており、直接対面で融資の相談をしたり、店舗で手続きを進めたりすることができます。また、青葉区には大手の街金から地元密着型の街金までさまざまな種類があり、ユーザーのニーズに応じたサービスを提供しています。オンラインサービスも多く、24時間利用できるため、便利に資金調達を行うことができます。

宮城野区

宮城野区も仙台市内で重要なエリアです。この区は仙台駅から近いため、アクセスが良好で、街金の利用者が多い地域です。仙台駅近くの商業エリアにある街金の店舗や、オンライン申込みで融資を受けることができるため、急な資金需要にも素早く対応できる環境が整っています。宮城野区内であれば、駅近で便利な立地を活かして、短時間で融資を受けることができるため、特に利便性が高いです。

太白区、泉区、若林区

仙台市内でも比較的住宅地が広がる太白区、泉区、若林区でも街金のサービスを受けることができます。これらのエリアでも、インターネットを利用した融資申込みが可能であり、オンラインを通じて時間を気にせずに申し込むことができます。特にインターネット申込みを利用すると、店舗に足を運ばずとも融資が受けられるため、忙しい人々にとって便利な選択肢となります。

仙台市外のサービス対象地域

仙台市内のエリアだけでなく、宮城県内の他の地域でも街金のサービスを利用することが可能です。特にインターネットを活用したサービスが広がっているため、仙台市外に住んでいる方々でも、仙台の街金から融資を受けることができます。

石巻市・気仙沼市

石巻市や気仙沼市は宮城県の北部や沿岸部に位置しています。これらの地域では、仙台市内の街金が提供するオンライン融資サービスを利用することができるため、急な資金需要にも対応可能です。オンラインで申し込みをすれば、石巻市や気仙沼市からも迅速に融資を受けることができ、便利にサービスを利用することができます。

名取市・大崎市

名取市や大崎市は仙台市から近く、都市圏として発展している地域です。名取市や大崎市に住んでいる人々も、仙台市内の街金のサービスを利用することができ、インターネットを通じてオンラインで申し込みを行えば、仙台市内の街金から融資を受けることが可能です。これにより、仙台市外に住む方々もスムーズに街金を利用できる環境が整っています。

街金を利用する際の手順

宮城(仙台)の街金を利用する際は、一般的に以下の手順で進めることができます。

1. オンラインでの申し込み

インターネットを通じて申し込む方法は最も一般的で便利です。ほとんどの街金では公式ウェブサイトから融資の申し込みができ、申込フォームに必要事項を入力します。オンライン申込みでは、名前や住所、収入に関する情報を入力し、簡単な審査が行われます。審査が通ると、指定した口座に融資金が振り込まれます。

2. 店舗での申し込み

店舗で申し込みを行う方法もあります。仙台市内の多くの街金には店舗があり、直接対面で融資の相談や手続きを行うことができます。店舗で申し込むと、スタッフと直接やり取りしながら条件や融資内容について確認することができるため、安心して利用できる方も多いです。

3. 審査と融資実行

申込みが完了した後、街金は迅速に審査を行います。審査が通れば、融資が実行され、即日または数日内に融資金が口座に振り込まれます。急な支払いが必要な場合、即日融資を利用することができるため、非常に便利です。

街金を利用する際の注意点

街金を利用する際にはいくつかの重要な注意点があります。

1. 金利について

街金の金利は一般的に銀行よりも高めに設定されています。急な資金調達が必要な場合でも、金利をよく確認してから利用するようにしましょう。金利が高いため、返済期間や返済額を計画的に考え、無理のない借り入れを心がけることが重要です。

2. 返済期日を守る

返済期限を守らないと、遅延損害金が発生し、返済が難しくなってしまうことがあります。返済計画をしっかり立て、返済期日を守ることが大切です。

3. 必要な額だけ借りる

急な出費に対応するために街金を利用する場合、必要以上に多く借りないようにしましょう。借りすぎると、返済が負担になり、最終的に経済的な厳しさが増すことがあります。必要最低限の額を借りるように心がけましょう。

宮城(仙台)の街金は、仙台市内だけでなく、県内各地でサービスを提供しており、オンライン融資を通じて多くの地域で急な資金調達が可能です。

インターネット申込みであれば、仙台市外からでも手軽に申し込むことができ、急な支払いに対応するために便利なサービスです。

利用する際には金利や返済期日について十分に理解し、計画的に利用することが大切です。

宮城(仙台)の激甘審査の街金を探すときの注意点

急な出費や生活費が足りない時に頼りになるのが、街金(消費者金融)です。

中でも「激甘審査」を謳う街金は、審査が緩いため、短期間でお金を借りられるという大きな魅力があります。

しかし、安易に利用すると後々トラブルになることもありますので、利用する際には慎重に判断することが求められます。ここでは、宮城(仙台)で激甘審査の街金を探す際に気をつけるべき注意点を詳しく解説します。

1. 街金の審査基準を理解する

激甘審査の街金だからといって、誰でも借りられるわけではありません。

審査基準は業者ごとに異なりますが、いくつかの基本的なポイントは共通しています。まずは、どのような基準で審査が行われているのかを理解しておきましょう。

収入や職業に関する条件

一般的に、街金は安定した収入があることを求めますが、激甘審査の街金ではその基準が若干緩く設定されていることもあります。

とはいえ、まったく収入がない場合や不安定な職業に就いている場合、審査に通過するのは難しくなります。いくら審査が甘いとはいえ、収入源が不明な場合や明らかに不安定な状況では、審査を通過するのは難しいと考えた方が良いでしょう。

信用情報の確認

審査の際には、過去の借り入れ状況や返済履歴もチェックされます。

激甘審査を謳う業者でも、借金が多すぎたり、過去に支払い遅延の履歴がある場合は、審査に影響が出ることがあります。無理に審査を通そうとすると、将来的に高い金利や厳しい返済条件を強いられることになりますので、過去の金融履歴を正確に把握し、その上で利用を検討することが重要です。

2. 高金利に注意

街金でお金を借りるときの最大の注意点は「金利」です。

特に「激甘審査」と謳う業者は、金利が高く設定されていることが多く、返済時に大きな負担となる可能性があります。契約を結ぶ前に、金利がどれくらいかを必ず確認しましょう。

金利の計算方法

街金の金利は、年利で表記されるのが一般的です。

例えば、年利18%の場合、100万円借りると1年後には118万円を返済しなければならないということになります。しかし、激甘審査を謳う業者では、金利が20%を超えることも珍しくありません。金利が高ければ、返済の負担も大きくなりますので、金利の設定が適正かどうかを事前に調べることが大切です。

返済の総額

金利が高いと、最終的に返済額が膨れ上がります。

例えば、10万円を借りて年利18%で1年後に返済する場合、支払う総額は118,000円となります。このように金利が高ければ、返済の負担はどんどん大きくなりますので、借りる金額や期間を慎重に決める必要があります。

3. 契約内容をよく確認する

契約を結ぶ前に、必ず契約内容を詳細に確認しましょう。

特に気をつけるべきポイントは、金利や返済条件のほかにも、以下のような内容です。

- 返済スケジュール: 返済方法が一括払いなのか、分割払いなのかを確認し、月々の返済額が自分の収入に見合っているかチェックします。月々の返済額があまりにも大きい場合、生活が困窮してしまう可能性があります。

- 延滞時のペナルティ: もしも返済が遅れた場合、どのようなペナルティが発生するかを確認することが大切です。延滞利息や遅延損害金が非常に高く設定されていることがあり、返済が遅れるとさらに多くのお金を支払わなければならないことがあります。

- 追加の手数料: 一部の街金では、借入時や返済時に手数料が発生することがあります。これらの費用についても契約前に確認し、隠れたコストがないかどうかを確かめましょう。

4. 返済能力を慎重に見極める

街金を利用する際、最も大切なのは「自分が無理なく返済できるかどうか」です。

激甘審査に通ったとしても、返済が難しくなると借金が膨らんでしまいます。返済能力を慎重に見極め、無理な借り入れを避けることが大切です。

返済計画の立て方

- 月々の返済額を計算する: 自分の月収や生活費を考慮した上で、返済額が無理なく支払える範囲内であることを確認しましょう。

- 生活費とのバランス: 生活費が足りないからといって、借り過ぎないように注意が必要です。必要最低限の金額だけを借り、生活費に困らないようにしましょう。

- 返済の余裕を持つ: 生活費の中で、返済額に余裕を持たせるようにしましょう。急な支出が発生した場合でも、返済に支障が出ないようにすることが大切です。

5. 口コミや評判をチェックする

実際に街金を利用した人たちの評判や口コミを参考にすることも、信頼できる業者を選ぶ上で非常に重要です。

インターネットやレビューサイトで、実際の利用者の体験談をチェックすることで、信頼性のある街金を見つけやすくなります。

良い口コミと悪い口コミの見極め方

- 良い口コミ: 返済のスムーズさや、迅速な対応についての口コミは信頼できます。また、顧客サービスやサポート体制がしっかりしている業者も評価が高い傾向にあります。

- 悪い口コミ: 返済が困難だったり、契約内容が不明瞭だったりする場合は注意が必要です。特に、業者が不正な手数料を取っていたり、金利が不透明な場合には警戒が必要です。

宮城(仙台)で激甘審査の街金を選ぶ際には、上述の注意点をしっかりと守り、冷静に判断することが大切です。

少しでも不安があれば、別の業者を選ぶか、他の金融機関を利用することを考える方が賢明です。

宮城(仙台)の激甘審査の街金は審査が甘い

宮城(仙台)の街金(消費者金融)は、審査が比較的甘いことで知られています。

これにより、急な資金が必要な際に非常に便利な存在となります。しかし、審査が甘いということは、簡単にお金を借りることができる反面、リスクも伴うため、利用する際には注意が必要です。この記事では、宮城(仙台)の激甘審査の街金がどのように運営されているのか、また利用する際の注意点について詳しく説明します。

街金(消費者金融)の特徴

街金とは、一般的に小規模な消費者金融のことを指します。

大手の銀行や消費者金融とは異なり、街金は柔軟な審査基準を採用することが多く、急な融資を希望する人々にとって利用しやすい金融機関です。

柔軟な審査基準

街金の最大の特徴は、審査が比較的甘いことです。

銀行や大手消費者金融では、安定した収入や勤務歴が重要視され、審査が厳しくなりがちです。しかし、街金ではこれらの条件が少し緩和されるため、アルバイトやパートのような不安定な雇用形態の人でも融資を受けることができる場合があります。審査に必要な時間も短いため、急な資金需要に対応しやすいという利点もあります。

少額融資が中心

街金では、少額の融資が中心となっています。

例えば、数万円から十数万円程度の融資が多く、少額融資を希望する人にとって非常に便利です。銀行や大手消費者金融では、融資額が多い場合には細かい審査が行われますが、街金は少額融資を中心に扱っているため、より早く融資を受けることが可能です。

高金利

審査が甘いということは、当然金利が高く設定されていることが一般的です。

街金の金利は、銀行や大手消費者金融よりも高めであるため、返済時にかかる利息が多くなりやすいです。急いでお金が必要だからといって、安易に借り過ぎてしまうと返済負担が大きくなることもありますので、金利については事前にしっかりと確認しておくことが重要です。

宮城(仙台)で街金を利用するメリット

宮城(仙台)においても、街金を利用するメリットは数多くあります。

特に、急な出費が必要なときに非常に役立つため、利用者にとっては魅力的な選択肢です。

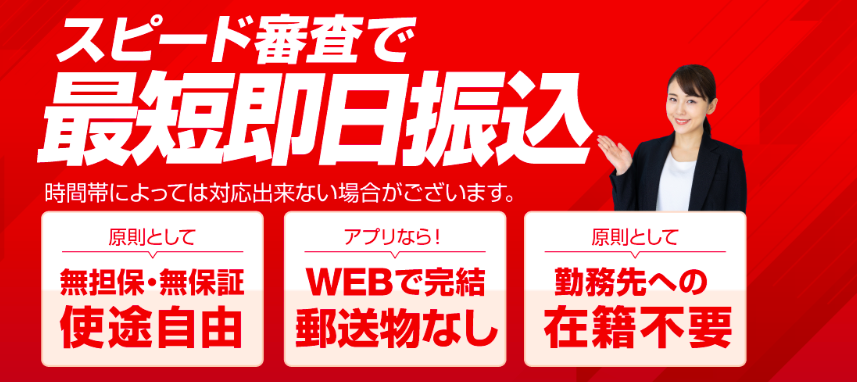

即日融資の可能性

街金では、即日融資を受けることができる場合があります。

審査が迅速で、申し込みから融資までの時間が短いため、急にお金が必要になった場合に非常に便利です。例えば、突然の病気や急な支払いが発生したときに、すぐに融資を受けられる点は大きなメリットです。

審査がスムーズ

銀行や大手消費者金融と比較して、街金の審査は非常にスムーズであることが多いです。

必要な書類が少なく、オンラインでの申し込みが可能な場合もあります。申し込み後、すぐに結果がわかることもあり、時間がない方にとって非常に便利です。

融資額の柔軟性

街金では、少額融資が中心となっていますが、必要に応じて融資額の調整が可能な場合もあります。

例えば、初めて利用する場合でも、少額から始めて、返済実績がついてから増額することができる場合があります。自分の返済能力に応じた融資額を選べる点は、借り手にとって非常に安心です。

宮城(仙台)の街金を利用する際のデメリット

一方で、街金を利用する際には注意点もあります。

審査が甘いという利点がある反面、デメリットも存在しますので、しっかりと把握しておくことが重要です。

高金利

街金の最大のデメリットは、金利が高いことです。

特に、短期間で融資を受けた場合、金利が積み重なることで返済額が膨らんでしまいます。利用前に金利を確認し、返済プランを立てておくことが大切です。高金利のため、長期間の返済になると、最終的に返済額が予想以上に大きくなることがあります。

返済負担

返済が遅れると、利息が増え、返済負担がさらに重くなります。

街金では、返済期日を守らないと、延滞金や追加の手数料が発生することがあります。こうした追加費用がかかることを避けるためにも、返済期日をしっかり守り、計画的に返済することが重要です。

借り過ぎのリスク

街金は審査が甘いため、つい借り過ぎてしまうリスクがあります。

必要な金額だけを借りるように心がけ、過剰に借り入れることは避けるべきです。借り過ぎると返済額が膨れ上がり、返済が困難になる可能性があります。借り入れは、自分の返済能力に応じて行うようにしましょう。

街金を選ぶ際のポイント

街金を選ぶ際には、いくつかのポイントを押さえておくと、より安心して利用することができます。

1. 複数の街金を比較する

一つの街金だけに決めるのではなく、複数の街金を比較して、自分にとって最も良い条件を選ぶことが大切です。

金利や返済条件、利用者の口コミなどをチェックして、納得できる街金を選びましょう。

2. 返済計画を立てる

借り入れをする前に、返済計画を立てておくことが非常に重要です。

返済能力を考慮し、無理なく返済できる金額を借りるようにしましょう。返済期日を守り、計画的に返済を行うことが、後々のトラブルを避けるためにも必要です。

3. 利用目的を明確にする

街金を利用する際には、借り入れの目的を明確にしておくことが重要です。

急な出費などの正当な理由であれば問題ありませんが、無駄な借り入れを避けるために、必要な金額をしっかりと計算してから申し込むようにしましょう。

宮城(仙台)の激甘審査の街金は在籍確認なしか

宮城(仙台)の街金(消費者金融)を利用したいけれど、在籍確認があることで少し不安を感じている方も多いかもしれません。

特に、プライバシーの問題や職場に知られたくないという理由で、在籍確認なしで融資を受けたいと考える方もいるでしょう。

実は、宮城(仙台)には激甘審査を提供している街金がいくつかあり、その中には在籍確認を行わないところも少なくありません。在籍確認がない場合、どのようなメリットやデメリットがあるのでしょうか?この記事では、宮城(仙台)の激甘審査を提供する街金における在籍確認について、わかりやすく解説していきます。

在籍確認の基本とは?

まず、在籍確認が何かについて簡単に説明します。

通常、消費者金融で融資を受ける場合、申し込み時に「在籍確認」が行われます。これは、申請者が本当にその職場に勤務しているかどうかを確認するための手続きで、主に電話を使って確認されます。電話を受ける際には、借り手の名前が告げられることなく、「その方は現在、勤務されていますか?」という形で質問されます。この確認を通じて、貸し手は収入が安定していることを確認し、融資を行うかどうかを決定します。

なぜ激甘審査の街金は在籍確認をしないのか?

宮城(仙台)の街金の中には、審査が非常に柔軟で、申し込んだその日に融資が決定する場合もあります。

なかでも「激甘審査」を売りにしている業者では、一般的な消費者金融が行う在籍確認を省略することがあります。その理由にはいくつかの要素があります。

1. 少額融資が多い

激甘審査を行う街金では、融資金額が比較的小額であることが多いです。

例えば、数万円程度の借り入れであれば、申請者の収入や職場情報を詳細に確認する必要性が低くなります。融資金額が少ないため、返済のリスクも少なく、審査が柔軟になり、在籍確認を省略しても問題ないと判断されるのです。

2. 迅速な対応を求められる

激甘審査の街金では、「即日融資」や「最短数分で融資」といったスピード重視のサービスを提供していることが多いです。

こうした業者では、在籍確認を行うとその分審査に時間がかかってしまうため、スピーディーな融資が難しくなります。そこで、在籍確認を省略することで、申し込んだその日や短時間で融資を受けることが可能になります。

3. プライバシー保護

在籍確認を省略する理由として、顧客のプライバシーを守るためという点もあります。

職場に電話がかかることで、借金の事実が知られるリスクを避けたいと考える利用者が多いです。特に、他人に知られたくない事情がある場合、在籍確認があると非常にストレスがかかります。そのため、プライバシーを重視する業者では、在籍確認を省略し、より安心して利用できる環境を提供しています。

在籍確認なしで融資を受けるメリット

在籍確認がない街金で融資を受けることには、以下のようなメリットがあります。

1. 職場に知られない

最も大きなメリットは、職場に借り入れのことが知られない点です。

在籍確認がないため、同僚や上司に融資を受けたことがばれる心配がありません。これにより、職場での人間関係やキャリアに影響を与えることなく、必要な資金を手に入れることができます。

2. 融資がスピーディ

在籍確認を省略することで、融資手続きが非常に迅速に進みます。

通常、在籍確認があると1〜2日かかることもありますが、激甘審査の街金では、申し込んだその日に融資を受けることができる場合も多く、急な資金が必要な際に非常に便利です。

3. 申し込み手続きが簡単

在籍確認がないため、申し込み手続きがスムーズに進みます。

職場への電話連絡を気にすることなく、必要な情報を提供するだけで融資が受けられるため、ストレスなく手続きを完了させることができます。

在籍確認なしで融資を受けるデメリット

一方で、在籍確認なしで融資を受けることには、いくつかのデメリットも存在します。

1. 高い金利が設定されることがある

在籍確認を省略することによって、貸し手側はリスクを背負うことになります。

リスクをカバーするために、金利が高めに設定されることが多いです。そのため、返済額が想定よりも大きくなる可能性があります。融資を受ける前に、金利や返済総額について十分に確認しておくことが重要です。

2. 融資額が限られることがある

在籍確認を省略することによって、融資額が制限されることがあります。

特に高額の借り入れを希望している場合、在籍確認なしでは融資額を十分に引き出せないことがあるため、その場合は他の金融機関を検討する必要があります。

3. 返済能力が見落とされる可能性

在籍確認がないため、借り手の収入状況や安定性を十分に確認できないことがあります。

これにより、返済能力を十分に考慮せずに融資が行われ、返済困難に陥るリスクが増す可能性もあるため、借り入れをする際には自己の返済能力をよく考えた上で利用することが重要です。

宮城(仙台)の激甘審査の街金は総量規制オーバーでも借りれるか?

宮城(仙台)の街金(消費者金融)は、しばしば「激甘審査」と称され、少しでも借り入れに不安がある人々にとって魅力的な選択肢となります。

しかし、総量規制が施行されていることをご存知でしょうか?

総量規制は、個人が借り入れられる総額を年収の3分の1までに制限するという法律です。

この規制は消費者金融に対しても適用されているため、総量規制を超える額を借りたい場合、果たして宮城(仙台)の街金で借りることができるのか疑問に思うかもしれません。

1. 総量規制とは?

総量規制とは、貸金業法に基づき、消費者金融を含む貸金業者が個人に対して貸すことのできる金額を、年収の3分の1までに制限する規定です。

この規制の目的は、過剰な借り入れを防ぎ、借り手が返済できない状況に陥るのを防ぐことです。

たとえば、年収300万円の人が総量規制を守る場合、最大で100万円までしか借りることができません。

すでに他の消費者金融で借りているお金があれば、その分が引かれます。すなわち、総量規制は、借り入れ額の合計が年収の3分の1を超えないようにするための制限なのです。

2. 街金(消費者金融)の激甘審査とは?

宮城(仙台)にある激甘審査の街金(消費者金融)では、審査が比較的緩いとされています。

これは、通常の金融機関と比較して、柔軟な対応をしている業者が多いからです。

具体的には、信用情報に傷があっても融資を検討してくれることがあり、過去に返済が遅れたことがある場合でも、状況によっては融資を受けられる場合があります。

とはいえ、激甘審査の意味が必ずしも「総量規制を無視して融資してくれる」というわけではありません。総量規制は、消費者金融にとっても法律で定められたルールであり、超過して借り入れることは難しいのです。

3. 総量規制オーバーでも借りられるケースとは?

宮城(仙台)の街金で総量規制を超えて借りる方法は、原則的にありません。

しかし、いくつかの特別な状況において、融資を受ける可能性が存在します。以下では、そのような状況や例外について詳しく解説します。

3.1. 配偶者の収入を合算する

総量規制は申込者自身の年収に基づいていますが、もし配偶者がいる場合、その配偶者の年収を合算して審査を受けることができる場合があります。

これにより、借り入れ可能な額が増えることになります。

たとえば、年収300万円の方が配偶者の収入を加算できる場合、年収500万円として計算され、これに基づいた融資額が算出されます。

この方法を利用すれば、規制を超えて借り入れができるかもしれませんが、配偶者の同意が必要であり、また配偶者の信用情報も審査対象となります。

3.2. 他の借り入れを完済する

もし他の金融機関での借り入れがあれば、それを完済することで借り入れ可能な金額が増えます。

たとえば、すでに100万円の借り入れがあり、その借り入れを完済すれば、その分だけ新たに借り入れができるようになります。

借り換えローンなどを利用すれば、低金利で返済額を減らしつつ、新たにお金を借りることも可能です。借り入れの総額が規制を超えない範囲であれば、この方法を使って融資を受けることができます。

3.3. 小額融資を受ける

一部の街金では、総量規制を守りながら少額融資を行っています。

総量規制内であれば、少額であっても融資を受けることができます。

この場合、月々の返済負担が少なくなるため、総量規制を超えた額を借りることが可能なケースがあります。

ただし、これもあくまで規制内での借り入れです。規制オーバーの場合は難しいと考えるべきです。

4. 激甘審査の街金でも総量規制を守る理由

宮城(仙台)の激甘審査を掲げる街金(消費者金融)でも、総量規制を守らなければならない理由は、法律で定められたルールだからです。

仮に審査を緩くすることで規制を超えて融資した場合、それが不正行為と見なされる可能性があります。

また、金融業者にとっても、貸し倒れリスクを避けるために規制を守ることが重要です。無理な融資を行うと、貸し倒れや返済の遅延が発生し、最終的には業者にとっても大きなリスクとなります。そのため、どんなに激甘審査を行っている街金でも、総量規制を遵守することが求められます。

5. 注意すべき点

総量規制オーバーで借りようとする際、いくつかの注意点があります。

5.1. 無理な借り入れは避ける

総量規制を超えて借りようとするのは、返済能力を超えた借金を背負い込むリスクがあります。

過剰に借りることは、最終的に返済が困難になる可能性が高く、延滞や自己破産を引き起こす原因となり得ます。無理な借り入れは避け、生活の中で本当に必要な額だけを借りるようにしましょう。

5.2. 返済計画を立てる

借り入れを行う際には、返済計画をしっかり立てることが重要です。

月々の返済額を現実的に設定し、無理なく返済できる額を借りることが必要です。

5.3. 信頼できる業者を選ぶ

激甘審査を掲げる業者は多いですが、信頼性に欠ける業者も存在します。

必ず金融庁に登録された業者を選び、契約内容をしっかり確認するようにしましょう。

宮城(仙台)の激甘審査の街金で即日融資を受けるには

急な支払いが発生したときや、予想外の出費に対応するために必要となるのが、即日融資を提供する街金(消費者金融)です。

特に宮城(仙台)の街金は「激甘審査」で知られており、審査が柔軟で、急いでいる人々にとって非常に便利な選択肢となります。

しかし、即日融資を受けるためには、ある程度の準備と理解が必要です。今回は、宮城(仙台)の街金で即日融資を受けるために押さえておくべきポイントを、初心者にも分かりやすく説明します。

1. 即日融資を受けるための準備

即日融資を受けるためには、申し込みの段階からしっかりと準備を整えておくことが大切です。

以下に、必要な準備を解説します。

1.1 必要書類の準備

まず、即日融資を受けるには必要な書類を準備する必要があります。

街金の審査では、主に以下の書類が求められます。

- 本人確認書類:運転免許証、健康保険証、パスポートなど

- 収入証明書:給与明細書や源泉徴収票など

- 住居確認書類:公共料金の請求書や住民票など

これらの書類をあらかじめ用意しておくと、申し込み後にスムーズに審査が進みます。

特にオンライン申し込みの場合、写真を撮ってアップロードすることが多いので、あらかじめデジタルデータを準備しておくと便利です。

1.2 オンライン申し込みの利用

宮城(仙台)の街金では、オンライン申し込みを受け付けているところが多いです。

オンライン申し込みは24時間いつでも行えるため、非常に便利です。

申し込みフォームに必要事項を記入し、必要書類をアップロードするだけで申し込みが完了します。これにより、店舗に足を運ばずとも簡単に融資を受けることができます。

2. 審査の流れとポイント

即日融資を受けるためには、審査を通過する必要があります。

街金(消費者金融)の審査は、他の金融機関よりも比較的柔軟で、通りやすいとされていますが、それでもいくつかのポイントがあります。

2.1 審査基準

審査基準は、主に以下の要素に基づいて行われます。

- 信用情報:過去にローンやクレジットカードの支払い遅延がないか

- 収入の安定性:定職に就いているか、安定した収入があるか

- 借入状況:他の借り入れが多くないか、返済能力に問題がないか

特に大切なのは、過去の信用情報です。

支払い遅延や滞納履歴があると審査に影響を与える可能性があるため、信用情報に問題がないかを確認しておくことが重要です。

2.2 返済能力の確認

街金は、申込み時に返済能力をしっかりと確認します。

安定した収入があり、無理のない借入額を希望している場合、審査が通りやすくなります。

収入証明書を提出することで、あなたの返済能力を証明することができます。もし過去に返済が困難だったことがある場合でも、街金によっては柔軟な対応をしてくれることがあります。

2.3 審査結果の通知

街金によっては、審査結果が数分から30分以内に通知されることが一般的です。

結果に納得すれば、そのまま契約を進めることができます。審査通過後に、融資の詳細や返済方法に関する案内が届きます。

3. 即日融資の流れ

即日融資を受けるためには、申し込みから融資実行までの流れを理解しておくことが重要です。

以下に、一般的な即日融資の流れを紹介します。

3.1 申し込み

オンラインで申し込みフォームに必要事項を記入し、本人確認書類や収入証明書をアップロードします。

申し込み内容に間違いがないように確認し、送信します。

3.2 審査

街金が申し込み内容をもとに審査を行います。

審査はオンラインで行われることが多く、通常は数分から30分以内に結果が通知されます。

もしも審査に通れば、融資の詳細や条件が案内されます。

3.3 契約

審査に通過した場合、契約の手続きを行います。

契約が完了すると、指定した口座に融資金が振り込まれます。

通常、振込は最短で数時間内に完了することが多いです。これにより、その日のうちに融資を受け取ることができます。

4. 即日融資を受ける際の注意点

即日融資を受ける際には、以下の点に注意することが大切です。

4.1 返済計画を立てる

即日融資を受けた場合、最も重要なのは返済です。

返済期日を守らずに延滞してしまうと、追加の費用が発生したり、信用情報に悪影響が出たりすることがあります。

返済計画を立て、返済をスムーズに行えるようにしましょう。

4.2 高金利に注意

街金の融資は、銀行などの金融機関と比較して金利が高めに設定されていることが多いです。

融資を受ける際には、金利をしっかり確認してから契約を行うようにしましょう。返済額が大きくなりすぎないように注意が必要です。

4.3 無理のない借入額

希望する融資額が自分の返済能力に合っているかをしっかりと考えましょう。

あまりにも大きな金額を借りると、返済が難しくなり、再度借り入れをしなければならない状況になってしまうことがあります。自分の収入と生活費に見合った借入額を設定することが重要です。

5. 即日融資をスムーズに受けるためのコツ

即日融資を受けるためには、以下のコツを押さえておくとさらにスムーズに進められます。

- 早めに申し込む:午前中に申し込みを完了させると、当日中に融資が振り込まれる可能性が高くなります。

- 書類を準備しておく:必要書類を事前に揃えておくと、審査がスムーズに進みます。

- 借入額を適切に設定:返済能力に見合った金額を申し込みましょう。

以上のポイントを押さえれば、即日融資をスムーズに受けることができるでしょう。

急な金銭的な困りごとにも、安心して対応できる手段として、街金の即日融資を活用しましょう。

宮城(仙台)の激甘審査の街金と、闇金との違い

宮城(仙台)には、激甘審査をうたった街金(消費者金融)がありますが、これは審査が比較的緩やかであることを意味しています。

しかし、この「激甘審査」を提供する街金と、まったく違法な存在である闇金には、明確な違いがあります。

どちらもお金を借りる手段として利用されることがありますが、その内容やリスクは大きく異なります。ここでは、宮城(仙台)の街金と闇金の違いを、わかりやすく解説していきます。

街金(消費者金融)の基本

街金は、正式には消費者金融と呼ばれ、法律に基づいて営業している金融業者です。

宮城(仙台)の街金も例外ではなく、消費者金融として必要な許可を得て運営されています。

街金は、一般的に個人向けの小額融資を行っており、迅速な審査と融資を提供することを特徴にしています。

1.1 審査基準の特徴

街金では、激甘審査を掲げるところもありますが、それでも借り手が完全に無審査でお金を借りられるわけではありません。

激甘審査とは、他の金融機関に比べて審査が柔軟であるという意味で、例えば過去に金融事故があった場合でも、融資を受けることができる可能性があります。

しかし、全く無条件でお金が借りられるわけではなく、収入の安定性や返済能力がしっかりと評価されます。

街金の審査は、以下のポイントをチェックします。

- 収入の安定性:一定の収入があるかどうかが審査の大きな要素です。

- 信用情報の確認:信用情報に問題がある場合でも、過去の履歴が改善されていれば融資が可能な場合があります。

- 返済能力:過剰な負担を避けるために、月々の返済額と収入のバランスを見ます。

このように、街金は柔軟ではあるものの、完全な無審査ではなく、借り手にとってもある程度の返済能力が求められます。

1.2 契約内容と金利

街金での融資契約は、明確な条件が記載された契約書に基づいて行われます。

法律に基づき、金利は年利20%を超えることはありません。

これにより、過剰な利息がつくことはなく、借り手にとっても返済計画を立てやすい環境が整っています。また、返済方法も多様で、一括返済や分割払いなど、利用者の都合に合わせて選ぶことができます。

闇金とは?

一方、闇金は全く別の存在であり、違法な金利や取り立て方法を用いてお金を貸し出す業者です。

闇金は、貸金業法を無視して金利を高額に設定し、法的に許されていない方法で借り手から金銭を徴収します。

宮城(仙台)には、闇金も存在しており、急な資金が必要な人々がそのリスクを知らずに利用してしまうことがあります。

2.1 高金利と返済の罠

闇金が提供する金利は、法定金利を遥かに超え、非常に高額になります。

年利は、100%以上になることも珍しくなく、借りたお金があっという間に膨れ上がり、返済が困難になります。

さらに、契約内容も不明瞭で、借り手に対して後から追加料金を請求したり、金利を急激に引き上げたりすることがあります。

返済の罠としては、以下の点が挙げられます。

- 利息の急激な増加:返済が遅れると、利息が急増し、元金を返すどころか利息だけで手いっぱいになることが多いです。

- 契約内容の不透明:契約書が曖昧で、貸し手が後から条件を変更して借り手に不利な契約にすることがあります。

闇金のような業者と契約してしまうと、返済のためにさらに借りることになり、借金地獄に陥る可能性が非常に高くなります。

2.2 違法な取り立て

闇金業者は、借金の回収においても非常に暴力的で違法な手段を取ることがあります。

遅延したり、支払いが滞ったりすると、電話や訪問を通じて脅迫や嫌がらせが行われ、最終的には暴力的な取り立てを受けることもあります。

これにより、借り手は精神的にも肉体的にも追い詰められ、最終的には身の安全を守るために警察に相談せざるを得ない場合もあります。

闇金業者は、合法的な取り立ての手段を一切使用せず、違法に取り立てを行うため、その利用者は大きな危険にさらされることになります。

街金と闇金の違い

街金と闇金には、法律に基づく運営と違法な運営の違いがあるため、利用者の安全性に大きな差があります。

以下に、それぞれの特徴を比較した表を示します。

| 項目 | 街金(消費者金融) | 闇金 |

|---|---|---|

| 法的運営 | 金融庁登録の合法な業者 | 無登録、違法な業者 |

| 金利 | 年利15%〜20%(法定金利内) | 年利100%以上(法外金利) |

| 審査基準 | 収入や信用情報を基に審査 | 審査なしで融資 |

| 返済方法 | 明確で計画的な返済方法あり | 返済方法が不明瞭、暴力的な取り立て |

| 契約内容 | 明確に契約書で示される | 契約内容が不明確、変更されることがある |

| 利用者保護 | 法的に保護される | 利用者の保護は一切ない |

どちらを選ぶべきか?

宮城(仙台)の街金は、法的に運営されており、融資の条件も明確で、適切に契約を結ぶことができます。

激甘審査を提供している場合でも、収入や返済能力をきちんと確認した上で融資が行われるため、借り手にとっても安心して利用できる点が多いです。

一方、闇金は法的に認められていない業者であり、その利用は非常に危険です。

高金利や違法な取り立てなど、利用者を不利益に追い込むことが多いため、闇金業者には手を出さないようにしましょう。

万が一、闇金に関与してしまった場合は、速やかに警察に相談することが最も重要です。

街金を選ぶ際にも、契約内容をよく理解し、返済計画を立ててから借りるように心がけましょう。

宮城(仙台)の激甘審査の街金で審査落ち・・お金を借りれないときは

急にお金が必要になった時、街金(消費者金融)に申し込んでみるのが一般的ですが、審査に落ちてしまうこともあります。

宮城(仙台)の激甘審査であっても、誰でも通るわけではないのです。

審査に落ちた場合、どのようにしてお金を借りることができるのか、考えるべきことや対処法を順を追って解説していきます。

1. 街金(消費者金融)の審査が通らない理由

街金の審査は、一般的に柔軟と言われていますが、審査に通るためにはいくつかの条件が必要です。審査に落ちた場合、まずはその原因を振り返ることが大切です。

1.1 信用情報に問題がある

信用情報は、銀行や消費者金融が最も重視する部分です。

もし過去にクレジットカードやローンの支払いが遅れた経験があったり、自己破産をしたことがある場合、信用情報に傷がついています。これが原因で、街金の審査に通るのが難しくなります。

1.2 収入が安定していない

街金は、借りたお金をきちんと返済できるかどうかを重視しています。

そのため、安定した収入があることが審査通過の条件となります。アルバイトやフリーランス、契約社員など、収入が不安定な職業だと審査が厳しくなることがあります。

1.3 借り入れが多い

すでに他のローンやクレジットカードで借り入れが多い場合、審査に通りにくくなります。

借金が多いと、返済能力を疑われるからです。特に、複数の金融機関から借り入れがある場合、返済に困る可能性があると見なされて、審査を通過できないことがあります。

1.4 必要書類の不備

申し込み時に提出する書類に不備があったり、虚偽の情報が記載されていた場合、審査に落ちてしまいます。

収入証明書や本人確認書類は正確で最新のものを用意しましょう。

書類不備は、審査を通るための基本的なハードルです。

2. 審査に落ちた場合の対処法

審査に落ちた場合でも、すぐに諦める必要はありません。

状況に応じてできることがあります。以下に、対処法をいくつか紹介します。

2.1 信用情報を確認し、改善する

信用情報に問題がある場合、まずは自分の信用情報を確認することが大切です。

信用情報機関に申し込みをすれば、自分の信用履歴をチェックすることができます。

万が一、記載ミスや誤情報があった場合は、訂正を依頼することができます。

信用情報の改善には時間がかかる場合もあるため、早めに確認し、必要な対応を取ることが重要です。

2.2 収入を安定させる

安定した収入がない場合、仕事を見直すことも考えてみましょう。

フリーランスやアルバイトの方で収入が不安定な場合、正社員として働くことを目指すと、収入が安定し、再度審査を受けたときに有利になることがあります。

安定した収入が確保できれば、街金での審査に通る可能性が高まります。

2.3 借り入れの整理

すでに他社から多くの借り入れがある場合、借金の整理を行うことを検討しましょう。

借り換えや債務整理を利用することで、月々の支払いを減らし、負担を軽くすることができます。

借り入れが減れば、返済能力が向上し、次回の審査に通過する確率が上がります。

2.4 必要書類を再確認する

審査に落ちた理由が書類不備の場合、提出書類を再度確認し、正確なものを用意しましょう。

収入証明書や本人確認書類が不十分だと、審査が進まないため、きちんと整った書類を準備することが大切です。

3. 審査に落ちた後の代替案

もし街金の審査に落ちたとしても、他にお金を借りる方法は存在します。

以下の選択肢を検討することができます。

3.1 銀行系カードローンを利用する

銀行系のカードローンは、街金と比較して金利が低いことが特徴です。

しかし、その分審査が厳しくなる傾向があります。もし街金で審査に落ちた場合でも、安定した収入がある場合は銀行系カードローンを試す価値があります。金利が低いため、返済負担が軽くなる可能性もあります。

3.2 質屋を利用する

質屋では、物品を担保にお金を借りることができます。

例えば、金やブランド品を持っていれば、その価値を元にお金を借りることが可能です。質屋では収入や信用情報に関わらず、担保がしっかりしていれば借り入れが可能です。急な資金が必要な場合には、選択肢として考えてみましょう。

3.3 親や友人から借りる

親や友人からお金を借りる方法もあります。

この場合、金利が発生しないことが多く、利息の負担を心配する必要がないため、最も負担が少ない方法です。ただし、返済計画をしっかり立て、口約束ではなく書面で契約を交わすことが重要です。

3.4 クレジットカードのキャッシング

クレジットカードにキャッシング機能がついている場合、それを利用する方法もあります。

審査が比較的簡単で、すぐにお金を借りることができます。ただし、金利が高いことがあるため、短期間で返済することを心掛けましょう。

4. 他の選択肢を検討する

審査に落ちた場合でも、お金を借りる手段は他にも多く存在します。

重要なのは、冷静に状況を見極め、最も適切な方法を選ぶことです。信用情報を改善したり、安定した収入を得ることで、再度街金でお金を借りるチャンスを得ることができます。また、質屋や親・友人から借りる方法、クレジットカードのキャッシングなどを検討し、無理なく返済できる方法を選ぶことが大切です。

自分の状況に合わせて、最良の選択肢を選びましょう。